PHEVs get room, but near-100% BEV scenario remains most likely

EV CHARGING

Gregory Jarry

1/21/20264 min read

The symbolic 100% CO₂ reduction target for 2035 is over: the European Commission now proposes a 90% cut, opening doors to PHEVs, e-fuels, and green steel offsets —while BEVs remain dominant. This analysis examines powertrain mix scenarios, PHEVs' transitional role despite real-world utility factor shortfalls and cost hurdles, and varying EU impacts —from near-100% BEV adoption in advanced markets to flexibility for Eastern Europe.

The European Commission has proposed major changes to the EU CO2 standards for light-duty vehicles

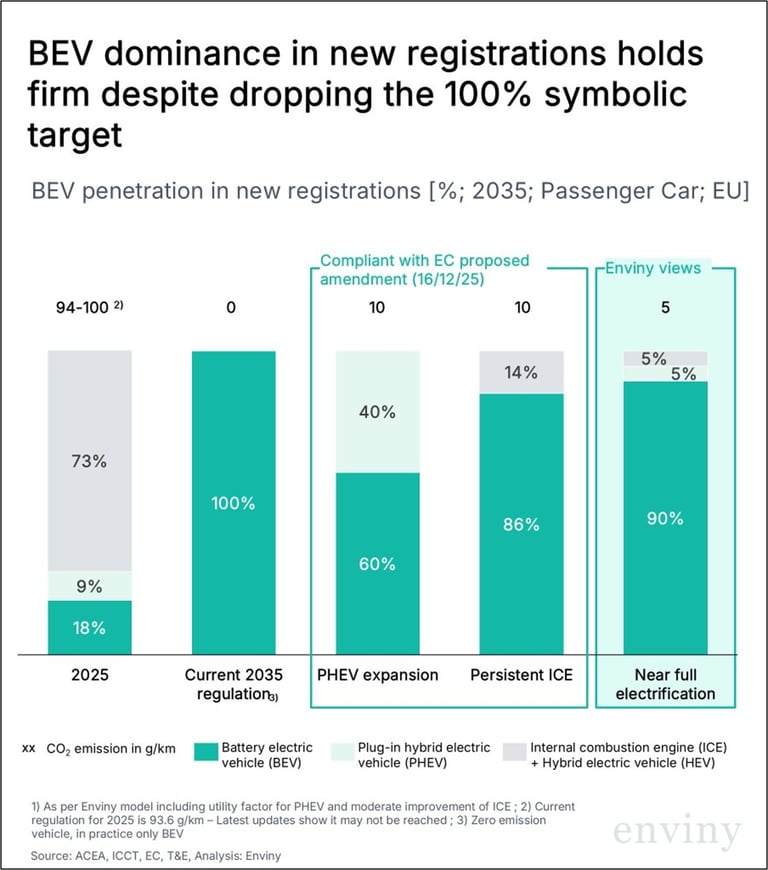

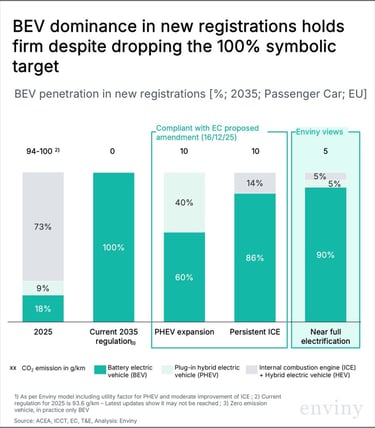

The 2035 target for new cars and vans shifts from a 100% CO₂ reduction (0 g/km) relative to 2021 to a 90% reduction, allowing a residual 10% of emissions (11 g/km for passenger car)

No restrictions on powertrain type for registered vehicles – unlike current regulation that mandates only zero-emission vehicles (BEV and FCEV)

Carmakers must compensate remaining emissions, or face penalties, via

renewable fuels (biofuel carbon correction factor): up to 3%

low‑carbon steel credits for green steel adoption: up to 7% – though green steel competitiveness remains uncertain

Several flexibilities are proposed on the way to 2035: super credits for small BEVs, 3-year averaging for 2030–2032 and weakening of the 2030 intermediate CO₂ targets for vans

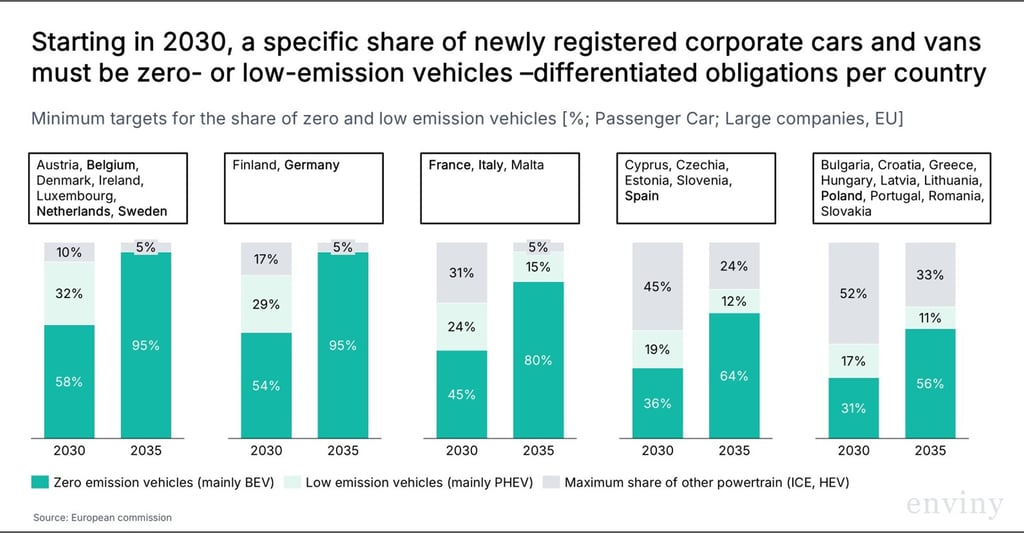

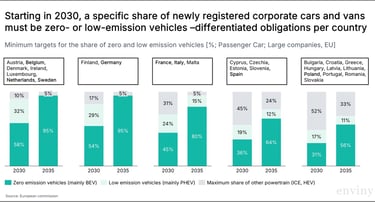

From 2030, a minimum share of newly registered corporate cars and vans must be zero- or low-emission (SMEs excluded). The European Commission sets differentiated quotas by EU countries, grouped into five clusters based on GDP per capita and national market maturity

In theory, diverse outcomes are possible depending on efficiency gains, PHEV utility factors and the level of offsets

Under the EU's proposed 90% CO₂ reduction target for 2035, BEV share in new passenger cars could range from 60% to 100%. In a PHEV expansion scenario, PHEVs could reach up to 40% share in 2035, assuming average WLTP CO₂ emissions of ~25 g/km per PHEV.

A strong penetration of BEVs appears to be the most plausible path given their growing cost‑competitiveness. Advanced markets should approach 100% BEV shares by 2035, while regulatory changes primarily support less mature markets, especially in Eastern Europe.

The proposed amendment creates more room for plug‑in hybrids, but they should remain a transitional solution

Plug‑in hybrids can ease the transition to electrification by cutting fuel use and CO₂ when regularly charged, while removing range anxiety for drivers not yet ready for a full BEV. They rely less on dense public charging networks, allowing many users to electrify a large share of their kilometers using mainly home or workplace charging.

However, PHEVs face major limitations:

The calculation of CO2 emission of PHEV in the overall performance of car manufacturers relies on a technical but crucial criterion: the share of electric km, so-called the utility factor. real‑world data (OBFCM) show that many PHEVs are charged less and driven in electric mode far less than assumed, leading to real emissions 3–5× higher than WLTP lab tests

PHEV is typically the most expensive of the three types of powertrains: the total cost of ownership hierarchy tends to be: BEV < ICE < PHEV for an average user, with PHEVs only becoming competitive in specific tax regimes and usage profiles with very high electric‑driving shares

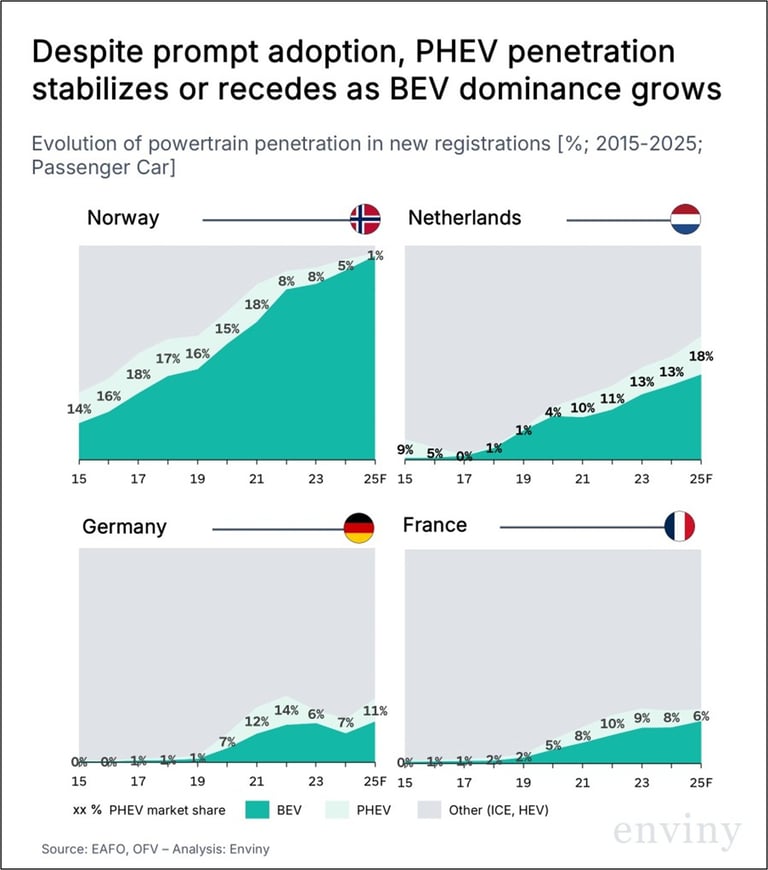

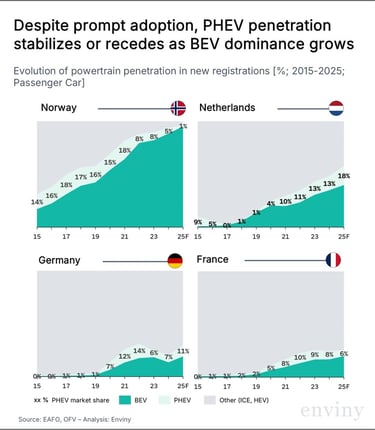

Market trends confirm PHEVs' bridging role: rapid early adoption fades as BEVs dominate post-transition

Enviny supports automotive investors and OEM partners in anticipating regulatory shifts and structuring powertrain transition roadmaps. Contact us to discuss how the 2035 CO₂ revision affects your strategy

Related insights

Feeding the AI Boom: Can data centers grow without burning more fossil fuels? | Enviny

Automotive transition: The future is electric, but how do we get there?

PHEVs get room, but near-100% BEV scenario remains most likely

EU's approach to decarbonizing the automotive sector - What is at stake?

Frequently asked questions

Q : What is the utility factor for PHEVs, and why does it matter?

The utility factor (UF) is the assumed share of kilometres driven in electric mode by a plug-in hybrid vehicle. The EU's WLTP methodology sets this at optimistic levels. Real-world OBFCM data show actual electric driving shares are far lower, meaning real emissions are 3–5× higher than type-approval values.

Q : What does the EU's revised 2035 CO₂ target mean for automakers?

The European Commission's 2026 proposal revises the 2035 target from 100% to 90% tailpipe CO₂ reduction versus 2021. This gives automakers flexibility to sell a limited share of PHEVs after 2035 — but the 90% threshold still effectively requires a dominant BEV share in the sales mix.

Q : Will PHEVs replace BEVs in the EU market after 2035?

No. Enviny's analysis concludes that a near-100% BEV market share remains the most likely outcome in leading EU markets by 2035. PHEVs may retain a niche role in specific segments, but the structural economics favor BEVs: falling battery costs, expanding charging networks, and OEM investment alignment.

Q : Which EU countries are closest to full BEV adoption?

Norway (already at over 90% BEV market share), Denmark, the Netherlands, Sweden, and Belgium lead the transition. Southern and Eastern European markets will likely reach the 2035 targets later and with a higher residual PHEV share.

Q : What is OBFCM and what does it reveal about real-world PHEV emissions?

OBFCM stands for On-Board Fuel and energy Consumption Monitoring — a mandatory EU data-collection system active since 2021. It reveals that most PHEVs are not charged regularly, and that their real-world CO₂ emissions are 3 to 5 times higher than WLTP values. This data directly informed the EU's decision to tighten the utility factor calculation.

Contact

© 2025. All rights reserved.

SOCIAL

ADDRESS

60, rue François 1er, 75 008 Paris, France