EU's approach to decarbonizing the automotive sector - What is at stake?

EV CHARGING

Gregory Jarry

9/16/20254 min read

The EU automotive sector and its extended EV ecosystem stand at a critical juncture. The Strategic Dialogue held on September 12 highlighted the urgent need for a cohesive EU framework and unified action to accelerate the automotive transition to EV, support innovation and strengthen Europe’s position in sustainable mobility.

Viewpoint #1 - What is at stake?

Last Friday, the third “Strategic dialogue on the future of the Europea automotive industry” took place. If all stakeholders agree that the future of road transport is electric, several voices are calling for a more flexible and pragmatic policy approach. What is at stake? What are the challenges? How might the outcome affect the automotive and energy sectors?

1. The future of automotive & energy industry

Millions of jobs across automotive, EV charging and energy sectors. The EU automobile industry alone accounts for c. 13 m jobs EUR 500 m, manufacturing 15 m vehicles, with a trade surplus exceeding EUR 81 bn last year

Infrastructure investment efficiency: Billions of euros have been invested or committed to EV charging infrastructure, battery and vehicle manufacturing, power generation and grid upgrades. As of Q1 2025, Europe has surpassed 1 million public charging points - with a growing share of ultra-fast charging – and another million should be installed in the next five years to meet EV charging needs. Similarly, the power sector has launched huge investment plans – EUR 60 to 70 bn yearly to make the EU grid fit for net-zero emissions

The competitiveness of European OEM: it has decreased over the last decade due to several factors: higher production costs, supply chain pressure, disruption by new entrants, slower innovation cycle / difficulty of managing the energy transition in a demanding regulatory context

2. Climate goals

Road transport accounts for ~ 20% of EU GHG emissions. All decarbonization plans foresee that these emissions will decrease significantly in the coming years, given that other sectors (aviation, industry, agriculture) do not have clear decarbonization paths for the moment and will decrease more slowly

Electrification appears as the only path to meet road transport decarbonization: other technologies are not as mature (H2) or do not have the same level of real-world emissions (PHEV, etc.).

3. Technological sovereignty

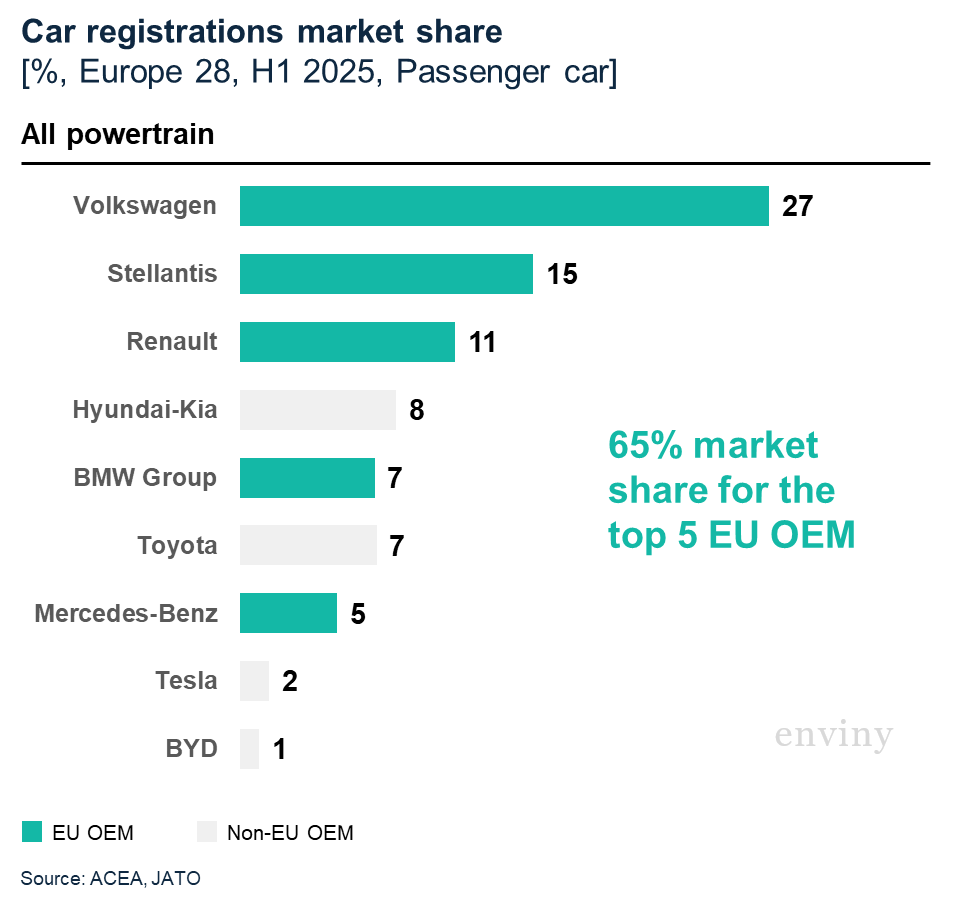

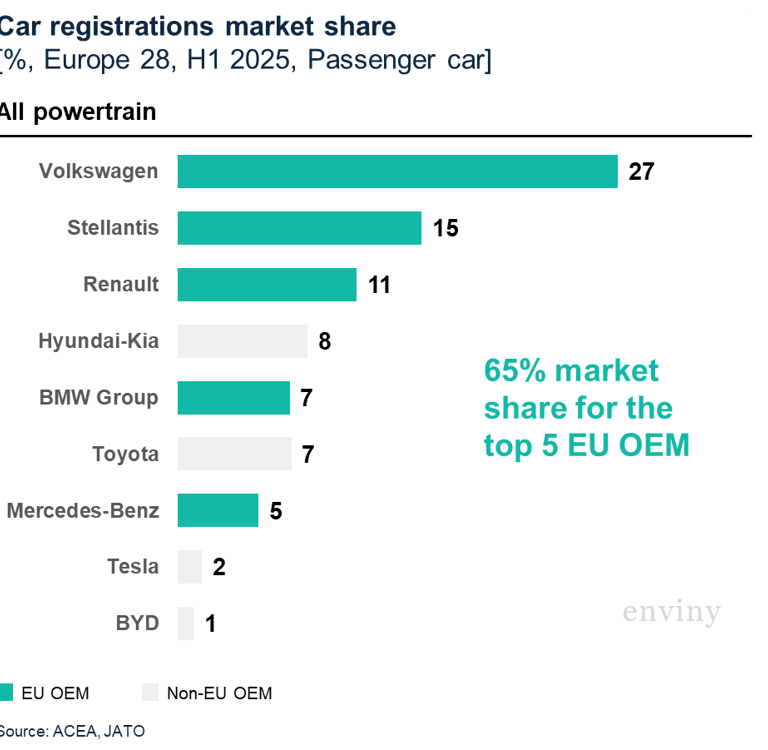

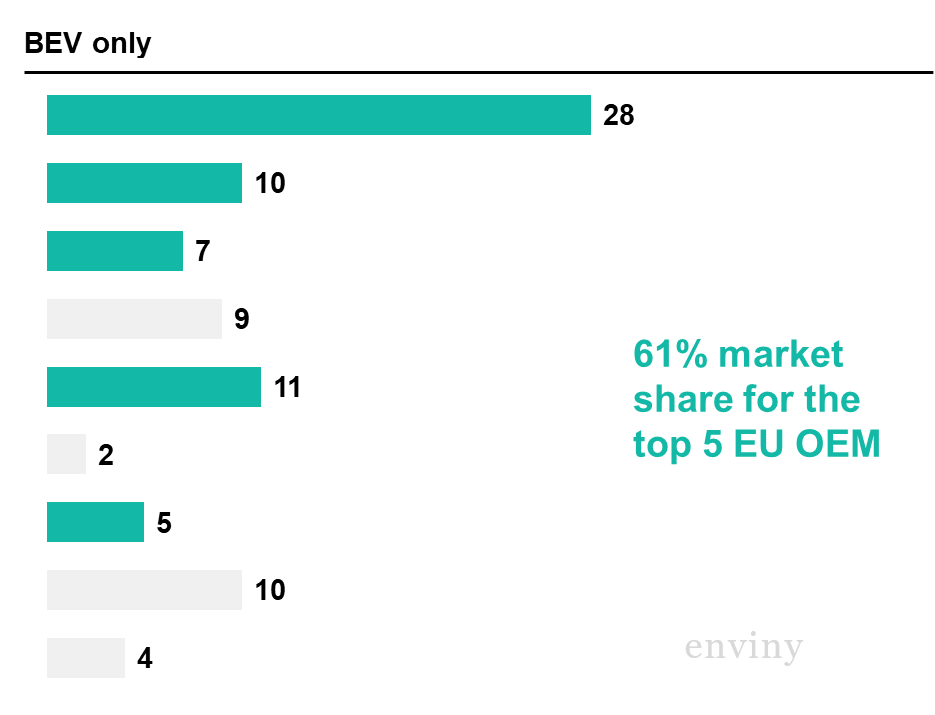

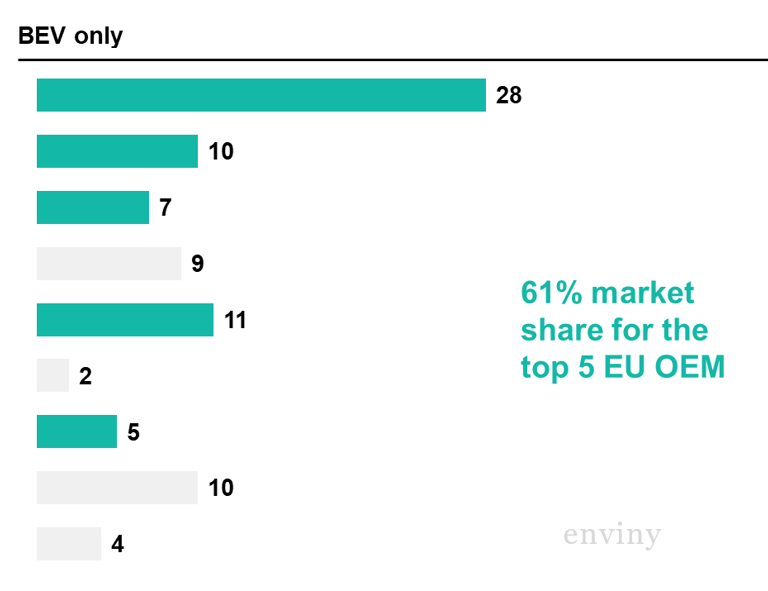

Sales of European EV OEMs are surging, though not all of them have reached their fair market share in Europe, while China and the US are getting more and more complex to address and new entrants are dominant globally (Tesla, BYD and other Chinese OEMs)

99% of batteries come from non-European manufacturers. Europe is currently outpaced at every step of the value chain. Building domestic battery production and supply chain capacities is a strategic imperative

Last but not least, the electric transition is a unique opportunity for Europe to reduce its dependency on imported crude oil while leveraging its low-carbon electricity capacities

Enviny advises investors and industrial players on EV transition strategies, from charging infrastructure to supply chain positioning. Contact us to explore how these scenarios apply to your business

Related insights

Feeding the AI Boom: Can data centers grow without burning more fossil fuels? | Enviny

Automotive transition: The future is electric, but how do we get there?

PHEVs get room, but near-100% BEV scenario remains most likely

EU's approach to decarbonizing the automotive sector - What is at stake?

Frequently asked questions

Q : What was the EU Strategic Dialogue on the future of the automotive industry, and why does it matter? The third EU Strategic Dialogue on the future of the European automotive industry took place on 12 September 2025. It brought together OEMs, suppliers, trade unions, and policymakers to assess the pace and conditions of the electric transition. Its significance lies in the scale of the stakes involved: the EU automotive sector represents approximately 13 million jobs and EUR 500 billion in output, with a trade surplus exceeding EUR 81 billion. While all participants agree the future is electric, several voices are calling for a more flexible and pragmatic regulatory timeline — making this dialogue a pivotal moment for the trajectory of EU climate and industrial policy.

Q : How significant are road transport emissions in the EU's overall climate agenda? Road transport accounts for approximately 20% of EU greenhouse gas emissions — making it one of the largest single contributors. Crucially, other high-emission sectors (aviation, heavy industry, agriculture) face greater technological and economic barriers to rapid decarbonisation. This means road transport must do more, faster. All credible EU decarbonisation scenarios project a sharp decline in road transport emissions over the next decade, driven almost entirely by the shift to electric vehicles.

Q : Why is full electrification considered the only viable path for road transport, not hydrogen or PHEVs? Hydrogen remains commercially immature for passenger vehicles: the infrastructure, cost, and energy efficiency challenges are unlikely to be resolved at scale within the 2035 regulatory window. PHEVs, meanwhile, fail to deliver their stated emissions reductions in real-world use: OBFCM data shows actual CO₂ output 3 to 5 times higher than WLTP values due to insufficient charging behaviour. Battery electric vehicles are the only technology that today combines scalable manufacturing, declining costs, and proven real-world emission reductions — which is why electrification remains the cornerstone of EU road transport policy.

Q : What is Europe's current position in battery manufacturing, and why is it a strategic concern? Europe is in a structurally weak position: 99% of EV batteries currently come from non-European manufacturers, predominantly Asian. European OEMs risk becoming assemblers of imported components — hollowing out domestic industrial value. Building competitive battery cell production and securing critical mineral supply chains is a strategic imperative, both for climate goals and for preserving Europe's industrial base. The EU's Battery Regulation and the European Battery Alliance represent steps in this direction, but the gap with Asia-Pacific players remains significant.

Q : How does the shift to EVs strengthen Europe's energy independence? Decarbonising road transport is not only a climate priority — it is an energy security play. Europe imports the vast majority of the crude oil consumed by its combustion-engine vehicle fleet, creating structural dependency on volatile global markets. Electrification redirects this demand toward electricity, much of which can be generated domestically from renewables and nuclear. For Europe — which leads globally in low-carbon electricity capacity — this is a strategic opportunity to reduce import dependency, stabilise energy costs, and leverage existing grid and generation assets.

Contact

© 2025. All rights reserved.

SOCIAL

ADDRESS

60, rue François 1er, 75 008 Paris, France