Automotive transition: The future is electric, but how do we get there?

EV CHARGING

Gregory Jarry

9/23/20254 min read

Scenario #1 - Delay or dilution of targets ➡️ A sector-wide decline expected for the mid to long term

Scenario #2 – Stand firm to 2035 objectives without adaptation ➡️ A world with leaders and left behind

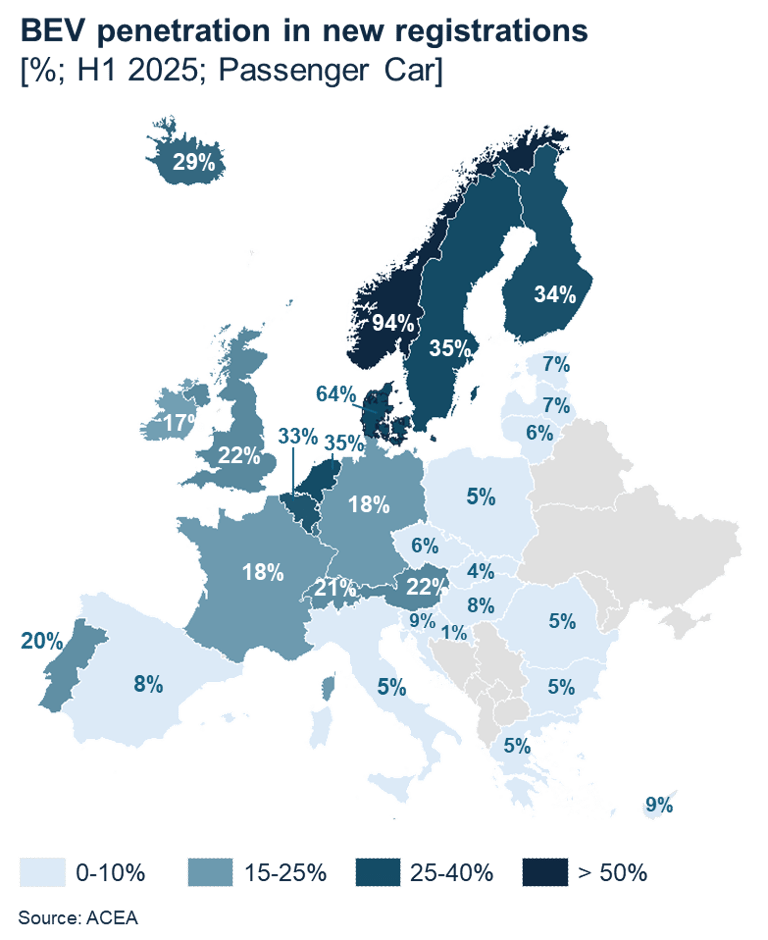

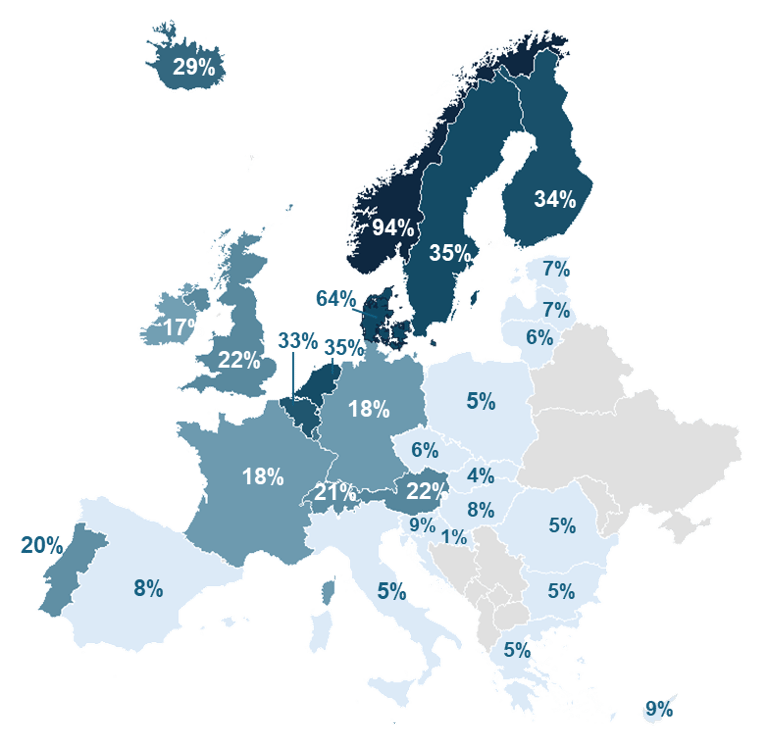

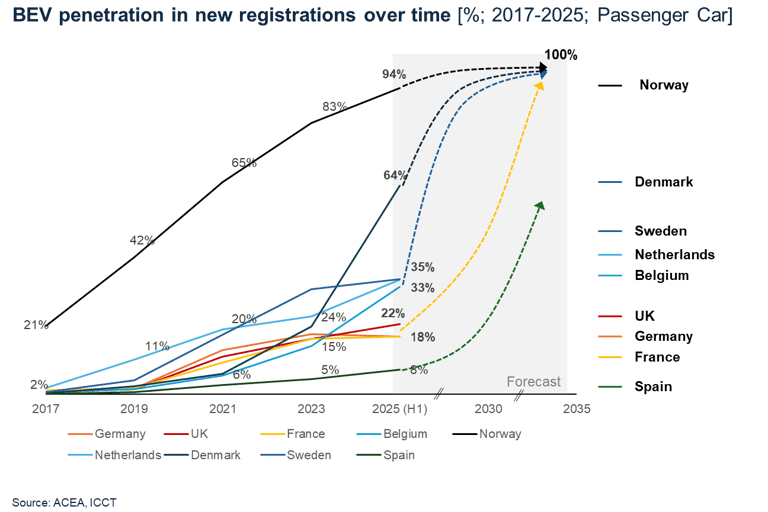

At the same time, the gap between early adopters and those left behind is widening. Electric vehicles are still in their infancy in most of Southern and Eastern Europe countries. Even in countries with a reasonable share of BEV in new registration (i.e. UK, Germany and France with BEV penetration around 20%), there is a long way to go to convince customers skeptical about innovation or with limited financial resources. Among the top concerns for potential buyers, higher upfront prices, range anxiety and lack of charging infrastructure are mentioned

Scenario #3 - Align climate objectives and policies with economic realities ➡️ The ambitious and inclusive path

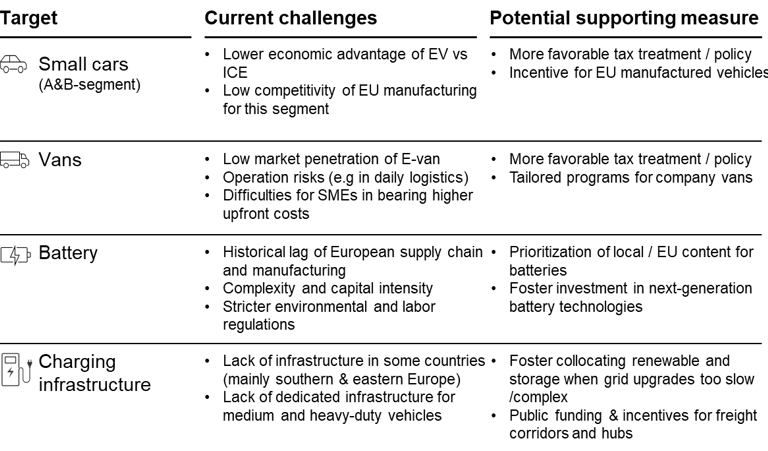

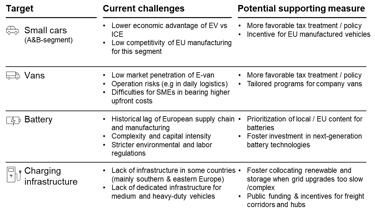

This approach keeps the existing targets of reduction of CO2 emissions for the different types of vehicles and focuses on the areas where the transition is the most challenged. Additional measures should be considered to help meet these goals, especially for smaller electric cars, vans, batteries, and charging infrastructure.

If the European targets and the local incentives have enabled the EV market to take off, it has created a multi-speed world. The adoption of EV has been very high in specific contexts:

> High sensitivity to the energy transition (early adopters / EV enthusiast, company frontrunners in sustainable practices, etc.)

> Strong purchasing power to support the higher upfront cost of the electric vehicle, and where the total cost of ownership is the key purchasing criteria

> Existence or ease of development of electrical/charging infrastructure

Hence EVs are already dominant, or nearly so, in Nordic countries and much of Western Europe, especially within corporate fleets and higher socio-professional groups.

Several voices coming from European car OEM and backed by politicians have been calling for renegotiating and diluting targets: postponement of the 2035 zero-emission target for cars and vans to 2040 or even further, reduction of penalties, non-binding target for vans, inclusion of alternative fuels / powertrains such as biofuels to power up ICE, plug-in hybrids or range extenders, etc.

👍 This scenario preserves the short-term margins of OEM procured by ICE and gives them more time to adjust their manufacturing capacities to raise the proportion of EV from 20% to 100%

👎 However, it compromises the long-term role of the European automotive and EV charging ecosystems in the electric world

> Maintaining innovation and manufacturing capabilities both for ICE and EV will increase pressure on the competitiveness of OEM and their suppliers

> Business plans of the EV charging players have been based on a steep increase of the utilization rate of the charging stations. A lower growth of the EV fleet will compromise both the profitability of the charging point deployed and the planned trajectory of future deployments (new stations and densification)

> In terms of technology sovereignty, the risk of dependency on non-EU players - already high - would increase dramatically: while Europe slows down, other markets like China have been accelerating, thereby speeding up the scaling of both their automotive and battery industries

In addition, backing down on this objective would undermine the credibility of the carbon neutrality targets announced for 2050.

Enviny advises investors and industrial players on EV transition strategies, from charging infrastructure to supply chain positioning. Contact us to explore how these scenarios apply to your business

Related insights

Feeding the AI Boom: Can data centers grow without burning more fossil fuels? | Enviny

Automotive transition: The future is electric, but how do we get there?

PHEVs get room, but near-100% BEV scenario remains most likely

EU's approach to decarbonizing the automotive sector - What is at stake?

Frequently asked questions

Q : What are the three scenarios for the EU automotive transition to 2035?

Enviny identifies three pathways. Scenario 1 (Delay and dilution): the 2035 target is repeatedly revised, creating regulatory uncertainty — the worst outcome for climate and industry. Scenario 2 (Stand firm): the 90% target is maintained uniformly, effective in leading markets but generating stress in lagging ones. Scenario 3 (Ambitious and inclusive transition): targets are maintained at EU level but implemented with differentiated national pathways and accelerated charging investment — Enviny's recommended scenario.

Q : Why is the BEV-dominant outcome still the most likely despite regulatory renegotiation?

Because the industrial logic is now locked in. European OEMs have committed hundreds of billions of euros to BEV platforms and battery gigafactories. The total cost of ownership of BEVs is converging with ICE vehicles in most European segments. The regulatory debate is about pace and fairness — not the ultimate destination.

Q : What is technology sovereignty in the context of the EV transition?

Technology sovereignty refers to Europe's capacity to master the key technologies of the electric vehicle value chain — primarily battery cells, electric motors, power electronics, and vehicle software. Today, Asian manufacturers dominate battery production, and European OEMs risk becoming assemblers of imported components. This is a central strategic concern of EU automotive policy.

Q : What are the main barriers to EV adoption in Europe?

Three main barriers: (1) upfront purchase price — BEVs still carry a 15–25% premium in most segments; (2) charging infrastructure gaps in rural areas and apartment-dense urban markets; (3) range anxiety, which reflects real limitations for long-distance users without reliable highway charging.

Q : How does the EU 2035 target compare to other major markets?

The EU's ambition is among the most stringent globally. The US has stepped back from binding federal ZEV mandates. China is pursuing aggressive EV deployment via industrial policy, with BEV + PHEV combined sales already exceeding 50% of the market. This context matters for European OEM competitiveness — making the design of the transition (speed, support measures, trade policy) critical.

Contact

© 2025. All rights reserved.

SOCIAL

ADDRESS

60, rue François 1er, 75 008 Paris, France